ENB Publishers Note: The Energy Crisis is one key component that has not been as big of a factor in past recessions. So as we look for Wall Street to determine if we are in a recession or not, the energy crisis will change how we will look at the charts and “Bull traps”.

Bloomberg – It’s been a chaotic, and costly, time for many investors. But 2022 is only half over and the stocks tale will probably have more twists and turns before the year is up.

Coming off the worst first-half since 1970, US equities now face a triple whammy of sticky inflation, recession risks and the threat to corporate profits from sinking consumer confidence. After just about everyone on Wall Street got their 2022 predictions wrong, investors are now focused on a toxic mix that spells stagflation, as well as more damage to valuations.

“The next 10% will probably be down from here, not up,” said Scott Ladner, chief investment officer at Horizon Investments. “A quick market bottom will need a turn in central bank policy, and we don’t think that’s a possibility in the next few months.”

Indeed, the Federal Reserve is expected to go on hiking rates as it tries to tame inflation, rather than flush the market with cash like it did in 2008 and 2020 — pretty much the rocket fuel for the powerful bull market that’s now come to a halt.

This year is already one of the worst in terms of big daily declines, with the S&P 500 Index falling 2% or more on 14 occasions, putting 2022 in the top 10 list according to data compiled by Bloomberg going back two decades.

Despite that, the CBOE Volatility Index, the so-called fear gauge, is below levels seen in past bear markets, suggesting the market has not yet seen the washout needed to spark a sustainable rally.

Based on the history of past bear markets, the S&P 500 should see some rebound by the end of 2022. In recession years, it’s a different story, with fresh lows to come first.

Michael J. Wilson at Morgan Stanley, one of Wall Street’s most vocal bears, says the S&P 500 needs to drop another 15% to 20% to about 3,000 points for the market to fully reflect the scale of economic contraction. For Peter Garnry, head of equity strategy at Saxo Bank A/S, the bottom is about 35% below January’s record high, implying further declines of about 17%.

“Companies such as Tesla and Nvidia, and cryptocurrencies, must capitulate before the speculative excesses have been eliminated and a bottom has been reached,” Garnry said.

Wall Street bulls see a better second half, though it won’t be enough to recoup all of the decline so far. In Europe, strategists in a survey expect the Stoxx 600 to post declines of 4% on the year. It’s currently down about 17%.

Earnings Test

Amid all the gloom, earnings estimates have remained relatively upbeat. That’s going to be tested when US and European companies start reporting second-quarter earnings in two weeks. Demand has so far held up even as consumer mood soured, but there have been signs recently that US spending is softening.

“Spending has been holding up because the gap has been bridged by savings built up during the pandemic,” said Anneka Treon, managing director at Van Lanschot Kempen. “And that is obviously unsustainable.”

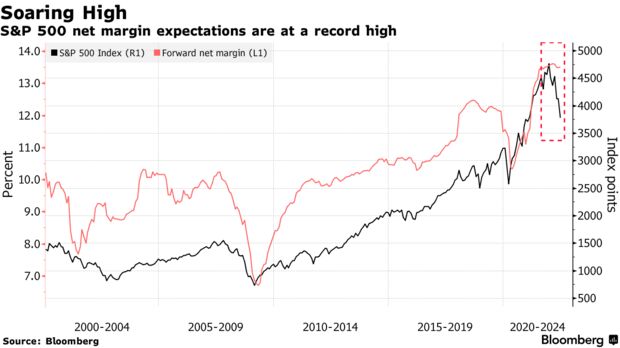

There’s plenty of scope for downgrades, with global profit-margin estimates seen as too optimistic. For Goldman Sachs Group Inc. strategists, margins for US companies will likely decline next year, whether or not the economy falls into recession.

In Europe, analysts for Stoxx 600 firms are the most bullish since 2001, according to Bloomberg data. And while a Citigroup Inc. index that tracks the relative number of earnings-per-share upgrades and downgrades shows the biggest US cuts since 2020, the number of European downgrades has only just started outnumbering upgrades.

Germany is among the markets at risk as Russia’s cuts to gas supplies threaten the industrial heart of Europe’s biggest economy.

Strong earnings expectations have made US and European valuations appear cheaper compared with long-term averages, tempting some investors to buy the dip and fuel short-term rallies. But when compared with bond yields, equities, in Europe at least, don’t look as cheap.

‘Inflation Inflation Inflation’

While the recession worries are on the increase, at the heart of the problem is runaway inflation. It’s continued to rise even as central banks take more aggressive steps, creating a one-two punch that could be a big part of the recession tipping point. Although there are some indications that peak inflation is near, central bankers are pushing on, having been accused of underestimating the threat at the start of the year.

“Inflation is at levels that many people have not experienced before and central banks are hiking rates to levels not seen since before the global financial crisis,” said Caroline Shaw, portfolio manager at Fidelity International. “Policy mistakes are likely and these can have a big impact on markets.”

In emerging markets, too, investors say they need to see the Fed turn less hawkish to ease concerns. That’s despite plunging valuations as stocks posted their worst first-half performance since 1998, when the Asian financial crisis upended markets and Russia defaulted. Hawkish central banks and slower economic growth will particularly pressure the tech-heavy, export-oriented markets of Taiwan and South Korea. Their respective stock benchmarks are among the biggest laggards in the region this year.

“Inflation inflation inflation,” said Ipek Ozkardeskaya, senior analyst at Swissquote. That “will determine whether we will see a U-turn before things get worse or whether the world should brace for deeper darkness through the second half of the year.”